A proxy model is the simplification of the full valuation model. It should be as close as possible to the full results. The proxy model is faster than the full model.

Application

The proxy model is likely to be used when the company has its own Internal Model and uses it instead of the Standard Formula. In that case, the company needs much more valuation results. For example, the company might need results for stresses on levels other than 1-in-200, stresses on pairs of risks, etc.

The proxy model might vary depending on the number of risks that it encompasses:

- approximation of all risks,

- approximation for part of risks and full calculation for others,

- approximation by individual risk.

Calibration

To calibrate the model, the company should determine the list of risk drivers.

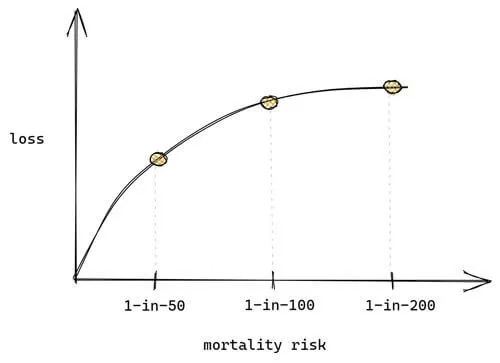

These could be equity, property, interest rates, inflation, lapses, mortality, expenses, etc. For each of the risks, the company should determine the level of stresses on which it will run the model, e.g. 1-in-10, 1-in-50, 1-in-200.

The company should also identify any material interactions, such as interest rates & longevity. The number of stresses might be higher for more material risks with difficult nature (e.g. non-linear).

The stresses should be for both: the beneficiary and adverse side, but the adverse side is more crucial. Then the full model should be run and the results should be used as data for calibrating the proxy model (e.g. fitting polynomials).