If you are an actuary, it is likely that you will come across the term Embedded Value (EV). Embedded Value is one of the reporting regimes - the set of rules of how to perform actuarial modelling and reporting.

In this post, we will present a short history of Embedded Value, its aim and main components. Before we start, it is worth mentioning that Embedded Value is not required by any regulators. The insurance companies are not obliged to publish results of EV (unlike for example Solvency II).

However, insurance companies might perform EV calculations for various reasons. The reason might be to report internal management information on profitability or to estimate an appraisal value when one company wants to buy another. The insurance company might also want to present the EV information to the public. EV is to some extent comparable to Solvency II. We present some reasons whether or not to calculate EV further in the post.

Aim

So, why does EV exist in the first place? EV is used to measure the value of the company from the perspective of the shareholders. Before EV, there were two types of published information: profit reporting and regulatory reporting. Profit reporting focused on a profit but only profit achieved over a year rather than long-term. Regulatory reporting showed results under prudent assumptions rather than realistic ones. There was a gap of information of what the company is actually worth. The gap was filled with EV.

Development

You might hear about few different types of EV, such as:

- Traditional Embedded Value

- European Embedded Value (EEV)

- Market-Consistent Embedded Value (MCEV)

Firstly, there was Traditional Embedded Value which used Achieved Profits Method. However, many companies used slightly different approaches to their calculations.

European Embedded Value was a further step to make the the EV results more comparable across companies. EEV was created during CFO Forum in 2004. There are 12 principles of EEV that are presented in the next section.

Still, the companies were using different approach especially to market assumptions and as a result Market-Consistent Embedded Value emerged in 2008/2009. MCEV basis is calibrated to a market valuation in a consistent way across firms. Further works on Embedded Value were stopped because Solvency II has been announced.

Embedded Value calculation

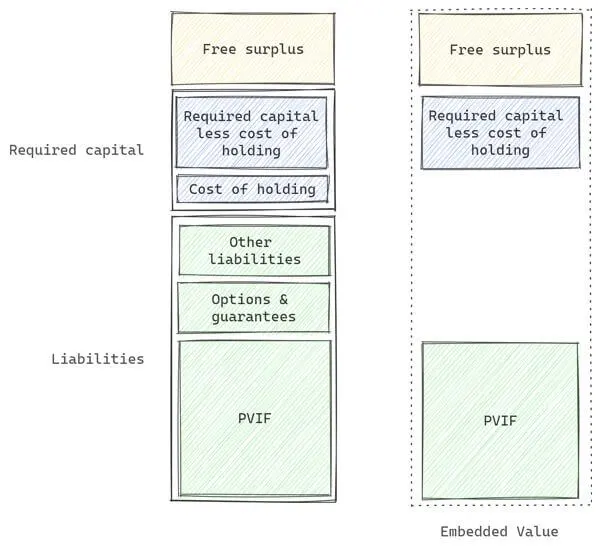

Embedded Value intends to measure realistic, risk-adjusted valuation of shareholder cash flows arising from in-force business and net assets. Embedded Value consists of three elements:

- present value of in-force business (PVIF),

- required capital less the cost of holding it,

- free surplus.

12 EEV Principles

- Principle 1

- Embedded Value (EV) is a measure of the consolidated value of shareholders' interests in the covered business.

- Principle 2

- The business covered by the EV Methodology (EVM) should be clearly identified and disclosed.

- Principle 3

- EV is the present value of shareholders' interests in the earnings distributable from assets allocated to the covered business after sufficient allowance for the aggregate risks in the covered business. The EV consists of the following components:

- free surplus allocated to the covered business,

- required capital, less the costs of holding required capital,

- present value of future shareholder cash flows from in-force covered business (PVIF).

- Principle 4

- The free surplus is the market value of any capital and surplus allocated to, but not required to support, the in-force covered business at the valuation date.

- Principle 5

- Required capital should include any amount of assets attributed to the covered business over and above that is required to back liabilities for the covered business whose distribution to shareholders is restricted. The EV should allow for the cost of holding the required capital.

- Principle 6

- The value of future cash flows from in-force covered business is the present value of future shareholder cash flows projected to emerge from the assets backing liabilities of the in-force covered business (PVIF). The value is reduced by the value of financial options and guarantees.

- Principle 7

- Allowance must be made in the EV for the potential impact on future shareholder cash flows of all financial options and guarantees within the in-force covered business. This allowance must include the TVOG based on stochastic techniques consistent with the methodology and assumptions used in the underlying embedded value.

- Principle 8

- New Business (NB) is defined as that arising from the sale of new contracts during the reporting period. The value of NB includes the value of expected renewals on those new contracts and expected future contractual alterations to those new contracts. The EV should only reflect the in-force business, which excludes future NB.

- Principle 9

- The assessment of appropriate assumptions for future experience should have regard to past, current and expected future experience and to any other relevant data. Changes in future experience should be allowed for in the value of in-force when sufficient evidence exists and the changes are reasonably certain. The assumptions should be actively reviewed.

- Principle 10

- Economic assumptions must be internally consistent and should be consistent with observable, reliable market data. No smoothing of market or account balance values, unrealised gains or investment return is permitted.

- Principle 11

- For participating businesses, the method must make assumptions about future bonus rates and the determination of profit allocation between policyholders and shareholders. These assumptions should be made on a basis consistent with the projection assumptions, established company practice and local market practice.

- Principle 12

- Embedded Value results should be disclosed at the consolidated group level using a business classification consistent with the primary statements.

To calculate or not to calculate

Embedded Value is not a required disclosure. The company should consider whether or not it brings value to perform EV calculations. In order to decide whether or not to continue publishing EV results, the actuaries should consider:

- the amount of additional work needed to calculate EV in terms of time, employees, computational needs, system requirements, audit controls, processes,

- who is the receiver of the results,

- what’s the additional value of publishing EV,

- what does the competition do,

- what are the expectations of shareholders and analysts,

- what value does analysis of change in EV bring,

- are there any recommendations from regulators or professional guidance.

If producing EV results does not require lots of additional work - and it shouldn’t, given the similarity to SII - and provides additional insight into the business, it might be worthwhile for the actuaries to produce these results.